Executive Summary

Persistent macroeconomic uncertainty, higher real interest rates, and waning confidence in the traditional 60/40 portfolio have prompted high-net-worth (HNW) investors to rethink capital allocation. Alternative investments—spanning private equity, private credit, real assets, infrastructure, commodities, and natural resources—offer not only diversification and inflation protection but also the potential for superior, uncorrelated returns.

This paper outlines how HNW investors can strategically integrate alternatives, leverage their structural advantages relative to institutions, and employ governance, tax, and risk frameworks to maximize success in a complex private-market landscape.

Market Context: A Structural Disconnect: Despite the deflation of speculative excess since 2022, global equity valuations remain historically elevated. As Jeremy Grantham has observed, markets sit within the top percentile of valuation extremes, even as real economic growth and productivity hover near historical lows. Simultaneously, higher baseline inflation and central-bank policy swings have eroded the safe-haven role of government bonds.

For multi-generational wealth, these trends reveal a new paradigm: consistent compounding and capital preservation now depend less on passive exposures and more on accessing less efficient, private-market opportunities that can generate alpha through structure, timing, and control.

Strategic Rationale for Alternatives in HNW Portfolios: High-net-worth investors occupy a unique middle ground—possessing both the flexibility of private entrepreneurs and access to institutional-grade strategies. Longer time horizons, fewer liquidity constraints, and access to bespoke deals enable them to capture structural premiums unavailable to retail portfolios.

Key Drivers:

• Inflation and Real Return Pressure: Persistent cost inflation compresses real yields. Real assets, commodities, and infrastructure can offer explicit or implicit inflation linkage.

• Market Volatility and Correlation Risk: The increasing co-movement between equities and bonds erodes diversification. Private assets often mitigate this by being driven by idiosyncratic or contractual cash flows.

• Low Forward Return Expectations: Consensus forecasts anticipate subdued nominal returns from public 60/40 portfolios. Private and real assets can enhance long-term total return while reducing cyclical drawdown risk.

The “new normal” calls for intentional illiquidity—allocating to private markets where control economics, structural alpha, and differentiated cash flow dynamics improve resilience.

Major Alternative Investment Categories

Private Credit: Private lending remains the foundation of many sophisticated portfolios. By financing lower- and middle-market enterprises underserved by traditional banks, investors capture contractual yields of 8–12%. Senior-secured, asset-backed, and mezzanine structures allow diverse risk-return positioning. Structured products—such as BDCs and SBICs—can deliver income streams and partial liquidity with institutional oversight.

Private Equity and Secondaries: Buyout, growth, and turnaround opportunities form the core of private equity allocations. Secondary funds provide access to seasoned portfolios at discounts, reducing the “J-curve” effect and improving early cash flows. For qualified investors, co-investments in single deals offer direct exposure without fund-level fees, enhancing net IRRs.

Real Estate and Real Assets: Real estate remains an anchor asset for HNW portfolios—whether through direct ownership, club deals, or value-add partnerships. Beyond housing or logistics, sectors such as data infrastructure, healthcare facilities, self-storage, manufactured housing and renewable energy storage combine stable income with long-term secular tailwinds.

Broader real assets—including timberland, farmland, and infrastructure—introduce inflation-hedged yield and real value preservation.

Infrastructure: Infrastructure investing—historically the domain of pension funds—is increasingly open to private investors through specialized partnerships, listed vehicles, and co-investments.

• Core infrastructure (toll roads, utilities, regulated assets) provides consistent, inflation-linked cash flows.

• Core-plus and value-add infrastructure (energy transition, digital networks, waste management) target mid- to high-teens IRRs with measured political and operational risk.

Commodities and Natural Resources: Commodities offer immediate inflation hedging and portfolio diversification due to their negative correlation with financial assets. Investors can access exposure through:

• Physical or futures-based strategies (energy, agriculture, metals) to capture cyclical or secular demand.

• Commodity-focused funds and royalties providing structured yield without storage or roll cost complexity (the mechanics of rolling contracts).

• Natural resource opportunities—such as oil & gas royalties, mineral rights, or carbon-credit funds—combine income, inflation protection, and long-term scarcity value.

These exposures function as real-return anchors within the “real assets” allocation sleeve, balancing deflationary shocks in financial markets.

Venture and Growth Capital: Innovation remains a vital asymmetrical opportunity set. Direct participation in AI, climate tech, or life sciences offers venture-scale upside, while growth-stage capital reduces binary risk. Disciplined diversification across 15–25 positions can target 20%+ expected IRRs.

Special Situations and Opportunistic Strategies: This flexible sleeve includes litigation finance, royalty streams, aviation or equipment leasing, distressed credit, and energy transition themes. These niche exposures often maintain low correlation to traditional market cycles and can enhance overall portfolio convexity.

Emerging and Frontier Opportunities: Tokenized Funds and Digital Access: Blockchain-native fund structures now provide fractional ownership and faster secondary liquidity, without altering underlying economics.

Private Secondaries Expansion: Online exchanges and platform-based liquidity windows shorten duration risk for traditionally illiquid strategies.

Impact and Sustainable Real Assets: Renewables, sustainable agriculture, and affordable housing funds blend attractive return profiles with measurable environmental and social alpha.

Institutional-Grade Governance for Private Wealth: Sophisticated private portfolios require institutional discipline. Key components include:

• Due Diligence: Assess manager pedigree, operational soundness, and alignment of interest.

• Transparency: Favor independent valuation agents and third-party fund administration.

• Liquidity Forecasting: Use capital call planning models to match inflows/outflows with spending horizons.

• Tax Management: Employ vehicles that mitigate UBTI exposure (CRT investing) and optimize estate outcomes through trusts, offshore feeders, “above the line” IDC deductions offered by oil and gas drilling.

• Regulatory Oversight: Stay abreast of SEC registration thresholds, cross-border restrictions, and qualified purchaser definitions.

Family offices now emulate endowments—integrating internal governance frameworks with specialized external advisory oversight.

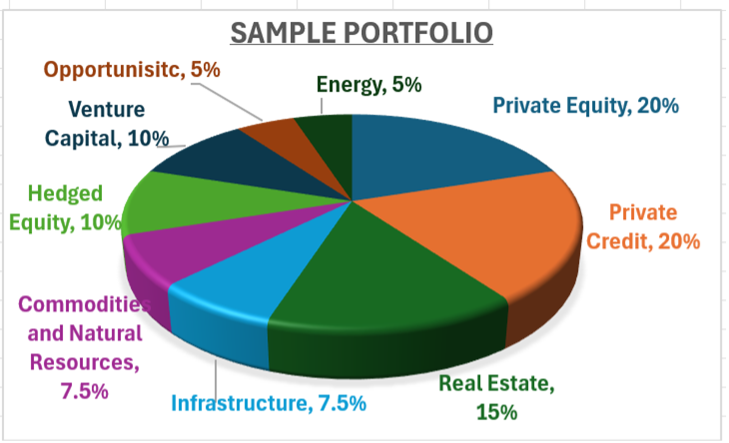

Model Portfolio Framework

An illustrative diversified alternative allocation for a high-net-worth investor might feature:

This construction balances income, growth, liquidity management, inflation protection and tax efficiencies—reflecting the structural advantages of HNW portfolios.

Key Takeaways

• The traditional 60/40 model faces structural headwinds; durable portfolios now require intentional private-market exposure.

• HNW investors can exploit flexibility, control, and longer-duration advantages unavailable to retail investors.

• Alternatives enhance inflation-resilience and reduce correlation.

• Institutional-quality governance, tax structuring, and liquidity planning safeguard long-term compounding.

• Emerging technologies and sustainable real assets will define the next generation of private wealth investing.

Conclusion

For modern wealth-holders, alternative investing is no longer peripheral—it is central to achieving resilience, preserving purchasing power, and compounding wealth through shifting cycles. Through disciplined governance, multigenerational alignment, and intelligent selection, investors can transform illiquidity into advantage.

Amadeus Wealth Alternatives continues to advance a pragmatic, research-driven approach—blending stable income assets with curated growth and innovation exposure—to help clients build portfolios capable of thriving through economic change.

Glossary of Terms:

• 2&20: Private funds often charge a 2% management fee and take 20% of the profits, often called the “carried interest” or “carry”.

• 40 Act: The securities act of 1940. We use the term to describe alternative investments which are registered with the SEC. They often have quarterly liquidity because they come in the form of an Interval Fund or BDC and can be custodied at a brokerage house.

• Asset Class: Broad category of investments. Alternative asset classes include: Private debt, private equity and real estate on a primary and secondary basis, promissory notes, equipment and aircraft leasing, direct and co-investments, venture investing, energy, options trading, multi-alternative, GP (General Partner) interests, litigation finance, mineral royalties, and other special situations.

• BDC: A business development company is a fund that invests in small and medium-sized companies as well as distressed companies. A BDC helps the small and medium-sized firms grow in the initial stages of their development. With distressed businesses, the BDC helps the companies regain sound financial footing. Set up similarly to closed-end fund, , many BDCs are typically public companies whose shares trade on major stock exchanges however they can be illiquid as well.

• Capital Calls: Many private funds frequently ask investors to send the commitment they’ve made to the fund over a period of years, ranging from all at once to up to 4-5 years.

• Co-investment: Where a private equity fund offers investors the opportunity to invest alongside the fund in a company they are acquiring, or lending to, but not through the fund, rather, as a direct investment, so often no fund level fees apply, like the 2&20 for example.

• Correlation: Refers to the behavior or one security or class of securities to another. If Stock A goes up 10% and stock B does the same, they are perfectly correlated and behave the same, a 100% correlation. If Stock A goes up 10% and Stock B goes down 10%, they are perfectly negatively correlated, so they do the opposite. Correlations range from -1 to +1, with a zero representing no correlation. The more non-correlated investments you have in a portfolio, the less volatile it will be. Alternative investments have low correlation to the stock market.

• Distribution to Paid-In Capital (DPI). A metric used to measure the return on investment for limited partners in a private equity fund, calculated by dividing the total amount distributed to investors by the total amount of capital they have paid into the fund.

• Illiquidity Premium: Investors of illiquid assets require compensation for the added risk of investing their funds in assets that may not be able to be sold for an extended period. Accordingly, illiquid investments can have higher returns than liquid ones over similar time horizons.

• Interval Fund: An interval fund is a type of pooled investment vehicle similar to a mutual fund that allows the issuer to repurchase fund shares from its shareholders at certain points in time, or intervals, allowing the investor to sell an otherwise illiquid investment, usually on a quarterly basis.

• J-Curve: The early years of a private equity investment are often negative, so the shape of the investment return looks like the letter “J”. A fund will acquire companies in years 1-3 of the fund’s life, improve them in years 4-7 and sell them in years 5-10, so the investor’s profits don’t materialize until later on. Meanwhile the 2% management fee is charged every year, so the returns are negative early on.

• Multiple On Invested Capital (MOIC). It is a metric used to measure the return on investment for a private equity fund or investment, calculated by dividing the total value of the investment (including any remaining unrealized value) by the initial amount invested. MOIC is often expressed as a multiple, such as 2x or 3x, indicating that the investment has returned two or three times its initial value.

• Opportunity Zone: A Qualified Opportunity Zone (QOZ) is an economically distressed community where private investments, under certain conditions, may be eligible for capital gain tax incentives, in particular, the deferral of capital gains until 2026. Opportunity Zones were created under the 2017 Tax Cuts and Jobs Act , signed into law by President Donald J. Trump on December 22, 2017, to stimulate economic development and job.

• Options: Options can be a CALL or a PUT. A CALL is a right to buy a security at a specific price and a PUT is a right to SELL. CALLs go up in value if the associated stock price rises and PUTs go up in value if they fall, similar to going “short”. Combinations of options in a “spread” are often used to hedge stock exposure in anticipation of a market decline.

• Private Credit: Like a private equity fund but using debt. A private debt fund will make loans to private companies.

• Preferred Return: Often 8%, although sometimes higher or lower, which the limited partner (LP) investor must earn before the general partner (GP) can take their carried interest.

• SBIC: A small business investment company is a type of privately-owned investment company that is licensed by the Small Business Administration (SBA). They have the potential to outperform owing to the leverage associated with the low interest loan the SBA provides to the fund.

• Secondary Investments: The purchase of a limited partnership from an investor who bought it years ago. For example, if the Yale University Endowment invested in a private equity fund years ago, and then decided they wanted to sell it today, how do they accomplish this given the fact the fund requires a ten-year commitment and is illiquid? There is a secondary market for these interests and many funds are established for the very purpose of buying these illiquid shares.

• Standard Deviation: a measure of the volatility of data including a portfolio’s return. It measures the extent to which returns vary above and below its average 68% of the time (one standard deviation) and 95% of the time (2 standard deviations). Given two portfolios with the same average return, the less volatile it is, the higher the value over time.

• UBTI: Unrelated business taxable income is income earned by a tax-exempt entity, such as an IRA, that is not related to the exempt purpose of the tax-exempt entity, thereby causing the IRA to have taxable income. This tax can be avoided by investing in an offshore vehicle sometimes offered by private funds since the offshore entity can block the UBTI.

• Waterfall: In the traditional waterfall structure, the GP receives carried interest after the invested capital and preferred returns have been paid back. This assures the GP will receive its carry early in the life of the fund. However, in the "European style" waterfall, GPs must pay back the invested capital on the investments liquidated as well as the invested capital on investments that have not been sold yet. This precludes the carry from being paid to the GP until the later years of the fund when all invested capital has been repaid back first.

• Warrants: Warrants are a derivative that give the right, but not the obligation, to buy or sell a security—most commonly an equity—at a certain price before expiration. They are sometimes issued to debt funds alongside their loans to private companies so the fund can participate in the appreciation of the company’s private stock.

Potential investors should be aware that an investment in Limited Partnerships involves a significant degree of risk and, therefore, should be undertaken only by investors capable of evaluating the risks of a Fund and bearing the risks they represent. In addition, there may be occasions when the Principals, General Partner, Advisor, Sub-Advisor and their respective affiliates may encounter actual and potential conflicts of interest with respect to a Fund. Prospective investors in a Fund should carefully read the Risks Section of a Fund’s Private Placement Memorandum and consider the information discussed therein which enumerates certain material risk factors and conflicts with respect to the Fund. If any of the events discussed in these sections occur, the Fund’s business, financial condition, results of operations and prospects could be materially adversely affected. In such cases, performance could decline, the Fund’s ability to achieve its investment objective could be negatively impacted and investors may lose all or part of their investment.